Artigo - ICEBERG DA SUSTENTABILIDADE ORGANIZACIONAL: a conexão entre aspectos visíveis e invisíveis

ICEBERG OF ORGANIZATIONAL SUSTAINABILITY: the connection between visible and invisible aspects

AMARAL, M. R. do; WILLERDING, I. A. V.; LAPOLLI, É. M. Iceberg of organizational sustainability: the connection between visible and invisible aspects. Aracê, [S. l.], v. 6, n. 4, p. 17873–17888, 2024d. DOI: 10.56238/arev6n4-399. Disponível em: https://periodicos.newsciencepubl.com/arace/article/view/2522

ICEBERG OF ORGANIZATIONAL SUSTAINABILITY: the connection between visible and invisible aspects

ICEBERG DA SUSTENTABILIDADE ORGANIZACIONAL: a conexão entre aspectos visíveis e invisíveis

ICEBERG DE LA SOSTENIBILIDAD ORGANIZACIONAL: la conexión entre aspectos visibles e invisibles

Abstract: This study aims to understand how environmental, social, and governance (ESG) practices can be integrated into organizations to promote organizational sustainability, addressing the urgent need for a systemic perspective on the relationship between humans, markets, and the environment. Employing a qualitative approach, the research was conducted through a literature review, identifying practices within the environmental, social, and governance dimensions that contribute to organizational sustainability. The study revealed that the balanced adoption of ESG practices strengthens organizations, enhancing their capacity to generate long-term value, manage risks, and improve efficiency. As a contribution, the Organizational Sustainability Iceberg Model was developed, classifying visible and invisible aspects of organizational sustainability. This research introduces a visual model to support organizations and researchers in the application of ESG practices, offering a structured perspective on the essential elements of organizational sustainability. The conclusions are limited to theoretical analysis, with empirical validation of the model recommended in different organizational contexts.

Keywords: Organization. ESG. Environmental, Social, and Governance Practices. Sustainability. Organizational Sustainability.

Resumo: Este estudo tem como objetivo compreender como as práticas ambientais, sociais e de governança (ESG) podem ser integradas às organizações para promover a sustentabilidade organizacional, abordando a necessidade urgente de uma perspectiva sistêmica sobre a relação entre seres humanos, mercados e o meio ambiente. Empregando uma abordagem qualitativa, a pesquisa foi conduzida por meio de uma revisão de literatura, identificando práticas nas dimensões ambiental, social e de governança que contribuem para a sustentabilidade organizacional. O estudo revelou que a adoção equilibrada de práticas ESG fortalece as organizações, aumentando sua capacidade de gerar valor a longo prazo, gerenciar riscos e melhorar a eficiência. Como contribuição, foi desenvolvido o Modelo Iceberg de Sustentabilidade Organizacional, que classifica os aspectos visíveis e invisíveis da sustentabilidade organizacional. Esta pesquisa apresenta um modelo visual para apoiar organizações e pesquisadores na aplicação de práticas ESG, oferecendo uma perspectiva estruturada sobre os elementos essenciais da sustentabilidade organizacional. As conclusões são limitadas à análise teórica, recomendando-se a validação empírica do modelo em diferentes contextos organizacionais.

Palavras-chave: Organização. ESG. Práticas Ambientais, Sociais e de Governança. Sustentabilidade. Sustentabilidade Organizacional.

Resumen: Este estudio tiene como objetivo comprender cómo las prácticas ambientales, sociales y de gobernanza (ESG) pueden integrarse en las organizaciones para promover la sostenibilidad organizacional, abordando la urgente necesidad de una perspectiva sistémica sobre la relación entre los seres humanos, los mercados y el medio ambiente. Empleando un enfoque cualitativo, la investigación se realizó a través de una revisión de la literatura, identificando prácticas dentro de las dimensiones ambiental, social y de gobernanza que contribuyen a la sostenibilidad organizacional. El estudio reveló que la adopción equilibrada de prácticas ESG fortalece a las organizaciones, aumentando su capacidad para generar valor a largo plazo, gestionar riesgos y mejorar la eficiencia. Como contribución, se desarrolló el Modelo Iceberg de Sostenibilidad Organizacional, que clasifica los aspectos visibles e invisibles de la sostenibilidad organizacional. Esta investigación introduce un modelo visual para apoyar a las organizaciones e investigadores en la aplicación de prácticas ESG, ofreciendo una perspectiva estructurada sobre los elementos esenciales de la sostenibilidad organizacional. Las conclusiones están limitadas al análisis teórico, recomendándose la validación empírica del modelo en diferentes contextos organizacionales.

Palabras clave: Organización. ESG. Prácticas Ambientales, Sociales y de Gobernanza. Sostenibilidad. Sostenibilidad Organizacional.

INTRODUCTION

The world is changing, and beyond profit, organizations are increasingly considering purpose and their impact on society, addressing environmental, social, and corporate governance issues. Sustainable development has gained importance, signaling a shift towards integrating sustainability criteria into business strategies (Amaral et al., 2023).

In this context, the concept of organizational sustainability is evolving, and this conceptual progress highlights environmental, social, and governance (ESG) practices, reinforcing an organization’s capacity to generate long-term value, improve efficiency, manage risks, and enhance competitive advantage through innovation (Belinky, 2021; Costa et al., 2022; Silva, 2023).

The literature reveals studies connecting ESG practices and organizational sustainability, though most focus primarily on environmental issues (Saxena et al., 2022). Furthermore, while many articles discuss the benefits of adopting these practices, they often fail to address how organizations implement them in a balanced manner or which specific aspects are impacted (Teles et al., 2015; Eccles et al., 2020; Senadheera et al., 2022; Amaral et al., 2023). This underscores the need for further research on the topic (Nunhes et al., 2020; Gillan et al., 2021; Nakagawa, 2023).

For this reason, it is necessary to understand how ESG practices can be adopted in a balanced way by organizations to promote organizational sustainability.

SUSTAINABILITY

The initial ideas about sustainable development emerged in the late 1950s, marking a transition from a solely economic focus, as advocated by Friedman (1979), to a broader perspective in which organizations prioritize not only profit but also social and environmental objectives, emphasizing the critical role of businesses within an integrated and interdisciplinary approach (Elkington, 2012).

In the 1980s, the United Nations’ Our Common Future report, also known as the Brundtland Report, introduced the concept of sustainability, defining it as the ability to meet current needs without compromising the ability of future generations to meet their own needs (UN, 1987).

During the 1990s, Capra (1996) and Elkington (2012) developed concepts offering alternatives to the traditional profit-maximization focus proposed by Friedman (1979). Both presented a more systemic perspective on sustainability, considering the interdependence of economic, social, and environmental factors. While Friedman viewed businesses as primarily economic agents, Capra and Elkington argued that companies should act as integral parts of a larger system, where their actions have significant consequences for society and the environment.

This led to the emergence of organizations pursuing sustainable actions, seeking a balance between economic viability and the conscious use of natural resources (Fialho et al., 2008). Additionally, there has been an increased need for businesses to adapt swiftly to new organizational models that are more flexible, emphasizing individuals’ interactions with society and decision-making transparency (Willerding, 2015).

The survival of humanity increasingly depends on a harmonious relationship with the environment, requiring cooperation and interaction among all living beings and their surroundings. This necessitates the adoption of a systemic, interconnected, and holistic view (Capra, 1996).

Thus, economic power should not be seen as the ultimate goal but rather as an instrument for achieving a balance among these factors (Panisson et al., 2017). Sustainability practices should transcend economic perspectives, assuming a central role in guiding businesses toward more sustainable (Esteves, 2021) and healthier practices (Amaralet al., 2023).

In this context, sustainability is critical for understanding the interactions between development and environmental preservation, as well as the interconnectedness of individuals and the impact of their actions on Earth.

ORGANIZATIONAL SUSTAINABILITY

Incorporating sustainability into business is closely tied to the concept of shared value, wherein companies can increase productivity along the value chain through sustainable practices (Porter, Kramer, 2011). When organizations focus solely on growth for profit without generating value, they may experience short-term growth but ultimately lose the ability to innovate, maintain customer focus, and sustain a long-term vision. It is essential to understand sustainability as a driver of value for all stakeholders (Mendes, 2012).

Stakeholder theory recognizes that organizations have obligations not only to shareholders but to all stakeholders. This is vital, as stakeholder pressure drives efforts to improve organizational outcomes (Gonçalves, 2014). Furthermore, organizations bear responsibility for the planet’s future and the well-being of upcoming generations (Alexandrino, 2020).

Organizational sustainability is associated with the ability to ensure long-term continuity and success (Vildåsenet al., 2017; Nunhes et al., 2020). Companies are considered sustainable when they adopt environmental, social, and corporate governance practices (Costa et al., 2022), generating benefits across various aspects of the organization and contributing to sustainable development (Teles et al., 2015).

The adoption of sustainable practices and the balance between environmental, social, and economic dimensions remain a topic of ongoing debate. Nevertheless, achieving this balance is a critical and urgent priority (Barrymore, Sampson, 2021; Delgado-Ceballos et al., 2023).

ENVIRONMENTAL, SOCIAL, AND CORPORATE GOVERNANCE (ESG) PRACTICES

With the growing adoption of environmental, social, and corporate governance (ESG) practices, it is evident that adopting the ESG perspective instead of the broader sustainability approach broadens the scope and optimizes initiatives, resulting in a more sustainable organization (Niemoller, 2021).

The implementation of ESG practices emerges as a fundamental strategy for organizational sustainability, enabling companies to minimize negative environmental impacts, promote equitable social relations, and ensure ethical and transparent corporate governance (Teles et al., 2015; Amaral et al., 2023).

The literature presents various practices related to the environmental, social, and governance dimensions of ESG. However, there is no consensus on which practices are most effective or appropriate for promoting organizational sustainability (Amaral et al., 2024). Table 1 summarizes the main environmental, social, and governance practices identified.

Table 1 – Environmental, social and governance practices identified in the literature

|

ESG Practices |

Authors |

|

|

Environmental Impact Assessment |

Garay; Font, 2012; Teles et al, 2015 |

|

|

Climate change, greenhouse gas mitigation, climate change adaptation, energy efficiency, and alternative energy sources for small and medium-sized enterprises |

Garay; Font, 2012; Teles et al, 2015; Niemoller, 2021; Costa et al., 2022; ABNT, 2022; Arco-Castro et al., 2023; Galindoet al., 2023 |

|

|

Water and effluent management |

Bandinelli et al., 2020; ABNT, 2022; Galindo et al., 2023 |

|

|

Conservation and sustainable use of biodiversity and soil |

Bandinelli et al., 2020; Cruz, 2021; ABNT, 2022; Galindo et al., 2023. |

|

|

Circular economy and waste management |

Garay; Font, 2012; Teles et al, 2015; Bandinelli et al., 2020; Cruz, 2021; ABNT, 2022; Galindo et al., 2023; Arco-Castro et al., 2023. |

|

|

Environmental management, air quality management, contaminated areas, and hazardous materials management |

Garay; Font, 2012; Costa et al., 2022; Cruz, 2021; ABNT, 2022; Galindo et al., 2023; Arco-Castro et al., 2023;. |

|

|

Territorial development, private social investment, stakeholder dialogue and engagement, and social impact |

Alvares; Souza, 2016; Chams, 2020; Cruz, 2021; Galindo et al., 2023; Garay; Font, 2012; Lee et al., 2016; Monteiro et al., 2021; ABNT, 2022; Amaral et al., 2023; Arco-Castro et al., 2023. |

|

|

Systematic inclusion of individuals or groups from surrounding communities as suppliers |

Galego-Alvarez et al., 2014; Amaral et al., 2023 |

|

|

Respect for human rights, elimination of forced or compulsory labor, and eradication of child labor |

Garay; Font, 2012; Alvares; Souza, 2016; ABNT, 2022; Amaral et al., 2023; Cruz, 2021; Galindo et al., 2023. |

|

|

Policies and practices for diversity, equity, and inclusion promotion |

Alvares; Souza, 2016; Chams, 2020; Cruz, 2021; Galindo et al., 2023; Garay; Font, 2012; Lee et al., 2016; Monteiro et al., 2021; Schleich, 2022; ABNT, 2022; Amaral et al., 2023; Arco-Castro et al., 2023. |

|

|

Fair labor relations and practices, professional development, quality of life, freedom of association, and remuneration and benefits policies |

Galego-Alvarez et al., 2014; Schleich, 2022; Cruz, 2021; ABNT, 2022; Amaral et al., 2023; Arco-Castro et al., 2023; Galindo et al., 2023. |

|

|

Occupational health and safety management |

ABNT, 2022; Schleich, 2022; Amaral et al., 2023 |

|

|

Promotion of social responsibility in the value chain and stakeholder engagement |

Garay; Font, 2012; Galego-Alvarez et al., 2014; ABNT, 2022; Schleich, 2022; Arco-Castro et al., 2023 |

|

|

Training and development policies within the value chain |

Schleich, 2022; Amaral et al., 2023 |

|

|

Corporate governance structure and composition, purpose, and strategy related to sustainability |

Garay; Font, 2012; Teles et al., 2016; Monteiro et al., 2021; Amaral et al., 2023; Arco-Castro et al., 2023; Cruz, 2021; ABNT, 2022; Galindo et al., 2023; IBGC, 2023. |

|

|

Business conduct, compliance, integrity programs, anti-corruption practices, prevention of unfair competition, and stakeholder engagement |

Monteiro et al., 2021; Cruz, 2021; Amaral et al., 2023; ABNT, 2022; Costa et al., 2022; Arco-Castro et al., 2023; Galindo et al., 2023; IBGC, 2023. |

|

|

Internal controls, business risk management, audits, legal and regulatory compliance, information security, and personal data privacy |

Teles et al., 2015; Cruz, 2021; ABNT, 2022; Galindo et al., 2023; IBGC, 2023. |

|

|

Transparency in management, accountability, ESG reporting, sustainability reporting, or integrated reporting |

Teles et al., 2015; Amel-Zadeh; Serafeim, 2018; Cruz, 2021; ABNT, 2022; Galindo et al., 2023; IBGC, 2023. |

Source: Prepared by the Authors (2024).

The adoption of social and environmental practices helps identify organizations with desirable and important characteristics for stakeholders (Niemoller, 2021). The Global Reporting Initiative (GRI) and the Brazilian Institute of Corporate Governance (IBGC) recommend integrating ESG aspects into organizational decision-making and strategic processes, as it is the responsibility of the organization’s top management to establish an environmental, social, and governance culture (GRI; IBGC, 2019). It is important to note that this journey is unique and varies for each organization (ABNT, 2022).

METHODOLOGY

This study is characterized as qualitative exploratory research, aiming to understand the meaning of a social or human problem (Creswell, 2010). Its objective is to explore how organizations can adopt ESG practices in a balanced manner to promote their sustainability. This article is part of the first author’s doctoral research, already presented to the qualification committee, under the supervision of the other two authors, who serve respectively as co-supervisor and supervisor.

A literature review was conducted with systematic searches in the Web of Science and Scopus databases using the terms “organizational sustainability” and “ESG practices,” along with searches in other data sources. From the selected documents, environmental, social, and governance practices were identified, which helped pinpoint aspects contributing to organizational sustainability.

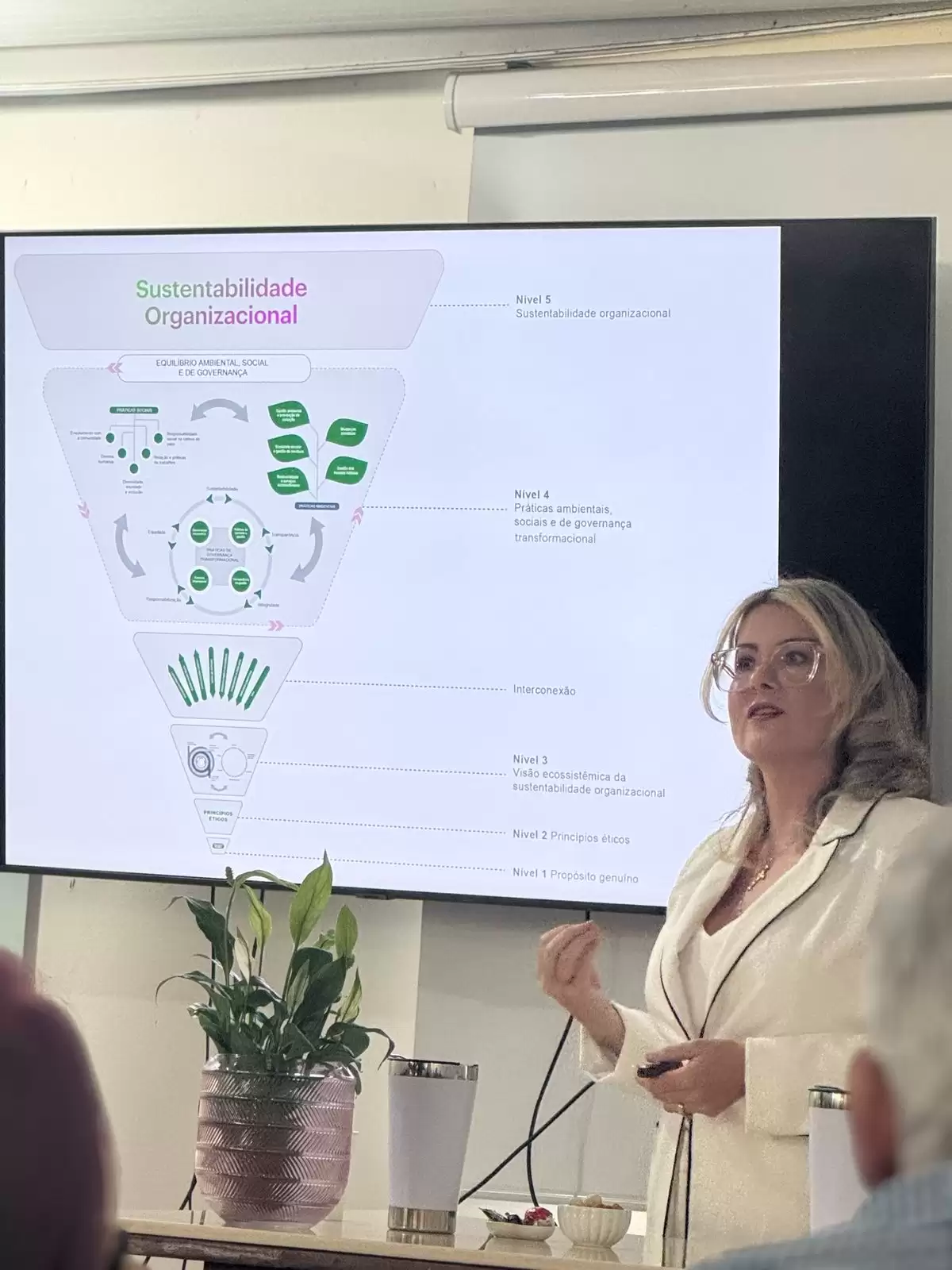

To meet the objective and represent the research findings, the study used an analogy with Edward Hall’s cultural iceberg model (1976). This model explains that only a small part of a culture is visible above the surface, such as language and behaviors, while the majority, including beliefs, values, and thoughts, lies submerged and invisible. This highlights the importance of being aware of these invisible aspects to fully understand a culture (Hall, 1976). Consequently, the Organizational Sustainability Iceberg was developed.

THE ORGANIZATIONAL SUSTAINABILITY ICEBERG

When applied to the organizational context, the visible aspects of an organization—such as policies, structures, and formal processes—can be illustrated. These aspects, although easily observed and measured, represent only the tip of the iceberg. A crucial portion that significantly influences organizational performance and competitive advantage lies below the surface, often deeply rooted and virtually impossible to quantify.

In Table 2, the visible and invisible aspects identified in the literature as determining factors for organizational sustainability are presented.

Table 2 – Visible and Invisible Aspects of Organizational Sustainability

|

Visible Aspects |

Invisible Aspects |

|

Healthy organization |

Entrepreneurial management |

|

Innovation |

Incentive structures |

|

Communication with stakeholders |

Sustainable internal policies |

|

Social initiatives |

Value generation |

|

Investor criteria |

Organizational resilience |

|

Sustainability reports |

Ethical behavior |

|

Sustainable products |

ESG balance |

|

Better outcomes |

ESG strategy |

|

Agenda 2030 |

ESG dimensions interdependence |

|

Environmental certifications |

Governance systems |

|

Strategic planning |

Competitive differentiation |

|

Diversity and inclusion |

Cultural transformation |

|

Entrepreneurship |

Purpose-driven priorities |

Source: Prepared by the Authors (2024).

The visible aspects represent practices and indicators that are easily measurable, while the invisible aspects reflect deeper and more subjective elements that permeate the organization’s purpose and culture, directly influencing strategic alignment with ESG principles and practices. The visible and invisible elements are interconnected with one another and among themselves, impacting each other and organizational sustainability at varying intensities. For better visualization, Figure 1 was developed.

Figure 1 – Relationship Network of Visible and Invisible Aspects

ESG 16.06.2025

ESG 16.06.2025